13 / 34

13 / 34

13

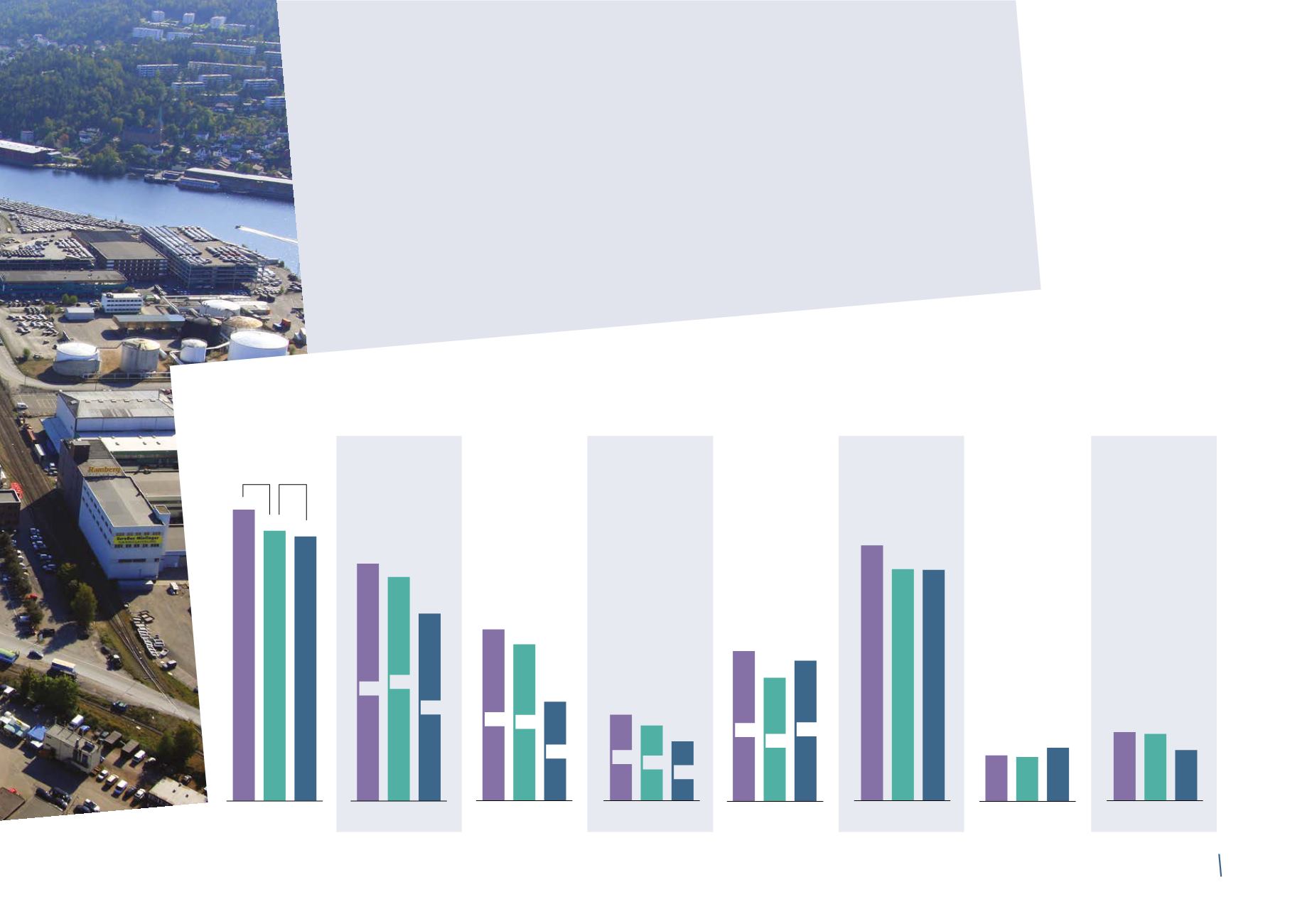

Capital expenditure rose to € 163 million in

2014, +20% vs. 2013. The main reason for the

increase is linked to the strategic Submarine

business, where investments to increase

production capacity and develop additional

technological capabilities were made at all

three production sites located in Arco Felice

(Italy), Pikkala (Finland) and Drammen

(Norway). Also of note was the upgrade of the

“Cable Enterprise” cable-laying ship which

Investing in high value-added businesses

will additionally boost the Group’s submarine

project execution capabilities.

A significant proportion of overall capital

expenditure was devoted to improving

efficiency in order to reduce fixed and

variable costs, with a focus on product design

and experimentation with new materials.

In the optical fibre field, the investment

programme to recover fibre manufacturing

competitiveness continued to move ahead.

2012 2013 2014

888

805

802

NET FINANCIAL

POSITION

ADJ. EBITDA

2012 2013 2014

650

613

509

8.6%

8.8%

7.4%

2012 2013 2014

494

465

365

ADJ. OPERATING

INCOME

2012 2013 2014

279

269

186

ADJ. NET PROFIT

2012 2013 2014

440

392

423

NET OPERATING

WORKING

CAPITAL

SALES

2012 2013 2014

7,574

6,995

6,840

-3.3% 1.8%

6.5%

6.7%

5.3%

3.7%

3.8%

2.7%

6.0%

5.8%

5.8%

2012 2013 2014

20.8%

20.3%

15.6%

ROCE

2012 2013 2014

139

136

163

CAPEX

Key financials

Amounts in millions of Euro - Percentages on sales

Note: Euro million

CAPEX