209 / 278

209 / 278

CONSOLIDATED FINANCIAL REPORT | EXPLANATORY NOTES

209

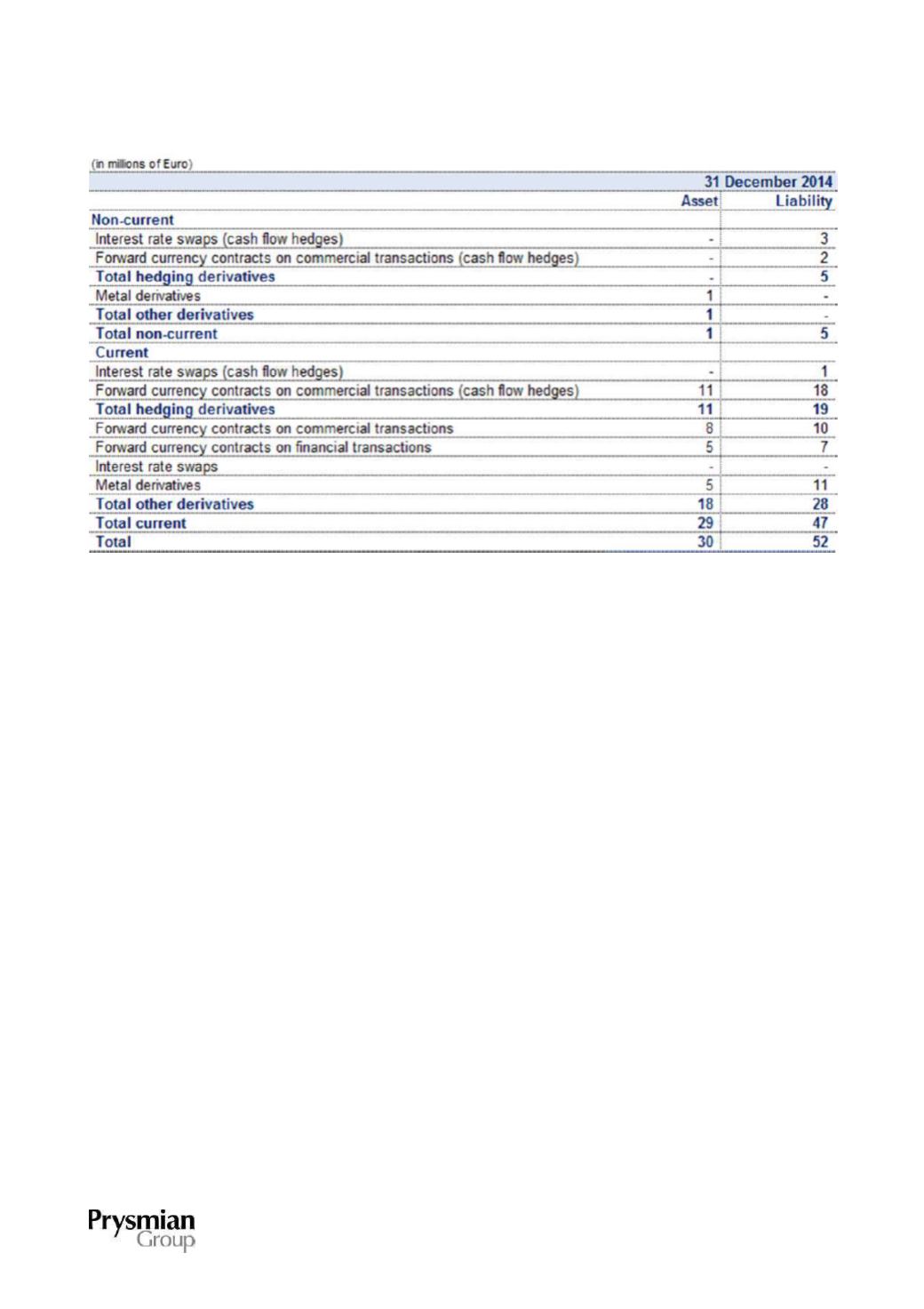

Interest rate swaps have a notional value of Euro 200 million at 31 December 2015 (the same as at

December 2014), and refer to derivatives whose hedge accounting was discontinued in 2014. These

financial instruments convert the variable interest rate component into a fixed rate of between 1.1% and

1.7%.

Forward currency contracts have a notional value of Euro 1,797 million at 31 December 2015 (Euro 1,679

million at 31 December 2014); total notional value at 31 December 2015 includes Euro 713 million in

derivatives designated as cash flow hedges (Euro 512 million at 31 December 2014).

At 31 December 2015, like at 31 December 2014, almost all the derivative contracts had been entered into

with major financial institutions.

Metal derivatives have a notional value of Euro 580 million at 31 December 2015 (Euro 523 million at 31

December 2014). The notional value for 2015 includes Euro 44 million for metal derivatives classified as

available-for-sale assets.

The following tables show the impact of offsetting assets and liabilities for derivative instruments, done on

the basis of master netting arrangements (ISDA and similar agreements). They also show the effect of

potential offsetting in the event of currently unforeseen default events: