203

The actuarial gains recognised at 31 December 2013 (Euro

1 million) mainly relate to the change in the associated

economic parameters (the discount and inflation rates).

Under Italian law, the amount due to each employee accrues

with service and is paid when the employee leaves the

company. The amount due upon termination of employment

is calculated on the basis of the length of service and

the taxable remuneration of each employee. The liability

is adjusted annually for the official cost of living index

and statutory interest, and is not subject to any vesting

conditions or periods, or any funding obligation; there are

therefore no assets that fund this liability.

The rules governing this liability were revised by Legislative

Decree 252/2005 and Law 296/2006 (Finance Act 2007):

amounts accruing since 2007 by companies with at least

50 employees now have to be paid into the INPS Treasury

Fund or to supplementary pension schemes, as decided by

employees, which now take the form of “defined contribution

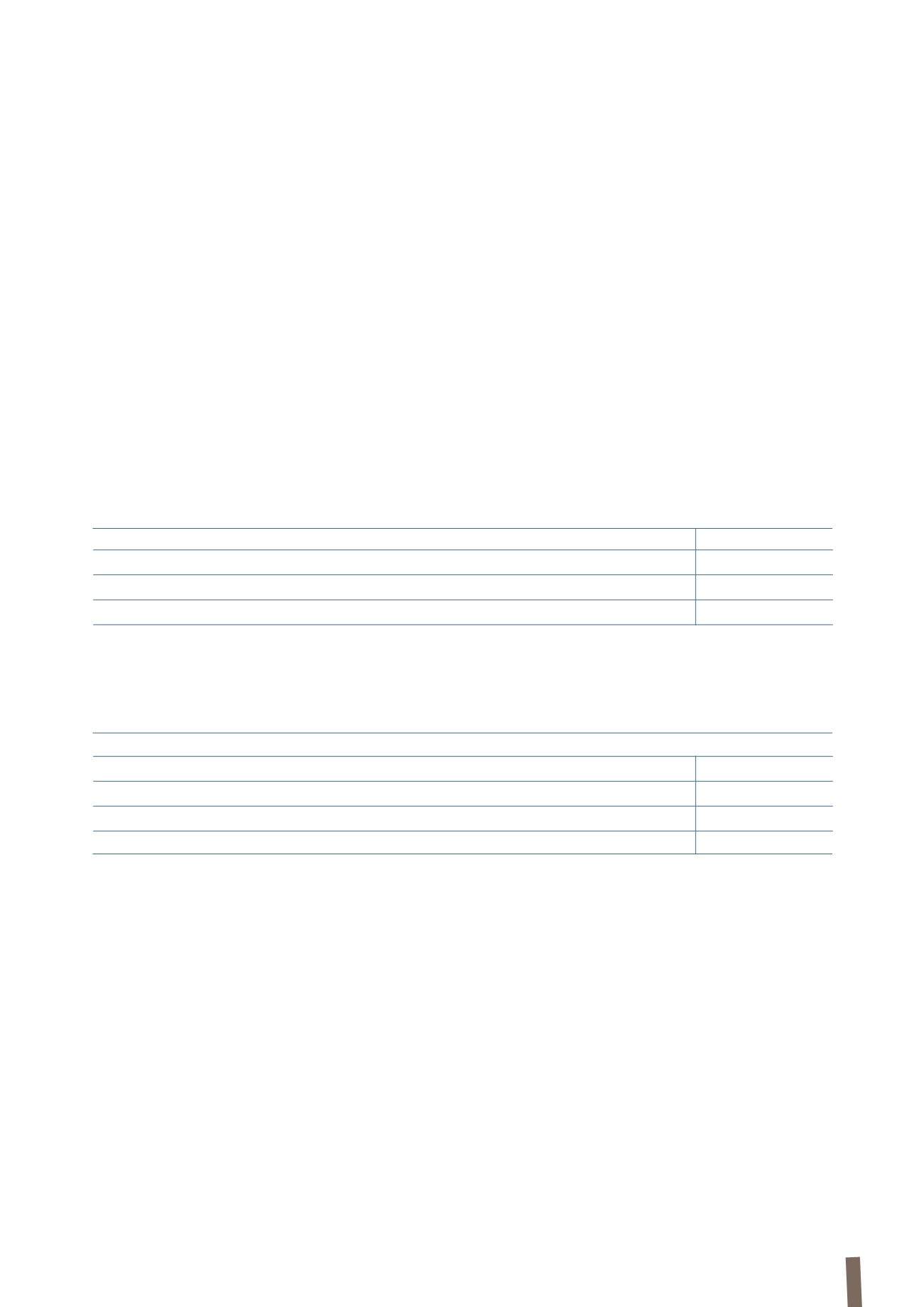

The following table presents a sensitivity analysis of the effects of an increase/decrease in the most significant actuarial

assumptions used to determine the present value of benefit obligations, namely the interest rate and inflation rate.

plans”. All the Group Italian companies nonetheless still

account for revaluations of amounts accrued before 2007,

while those companies with fewer than 50 employees

continue to accrue amounts in respect of this liability that are

not intended for supplementary pension schemes.

The benefits relating to this plan are paid to participants in

the form of capital, in accordance with the related rules. The

plan also allows partial advances to be paid against the full

amount of the accrued benefit in specific circumstances.

The main risk is the volatility of the inflation rate and the

interest rate, as determined by the market yield on AA

corporate bonds denominated in Euro. Another risk factor

is the possibility that members leave the plan or that higher

advance payments than expected are requested, resulting

in an actuarial loss for the plan, due to an acceleration

of cash flows.

The actuarial assumptions used to value employee indemnity

liability are as follows:

31 December 2013

31 December 2012

Interest rate

3.00%

2.75%

Expected future salary increase

2.00%

2.00%

Inflation rate

2.00%

2.00%

31 December 2013

decrease - 0.50%

increase + 0.50%

Interest rate

+5.23%

-4.80%

decrease - 0.25%

increase + 0.25%

Inflation rate

-2.58%

+2.64%

MEDICAL BENEFIT PLANS

Some Group companies provide medical benefit plans for

retired employees. In particular, the Group finances medical

benefit plans in Brazil, Canada and the United States. The

plans in the United States account for approximately 80% of

the total obligation for medical benefit plans.

Apart from interest rate and life expectancy risks, medical

benefit plans are particularly susceptible to increases in the

cost of meeting claims. None of the medical benefit plans has

any assets to fund the associated obligations, with benefits

paid directly by the employer.

As noted earlier, the US medical benefit plans account for the

majority of the benefit obligation. These plans are not subject

to the same level of legal protection as pension funds. The

enactment of important health care legislation in the United

States (the Affordable Care Act, also known as “ObamaCare”)

could result in a reduction of costs and risks associated with

these plans, as plan members move to individual forms of

insurance. Currently the new reform has had no impact on

liabilities and costs.