151

• Euro/British Pound: in relation to trade and financial

transactions by Eurozone companies on the British market

and vice versa;

• Euro/US Dollar: in relation to trade and financial

transactions in US dollars by Eurozone companies on the

North American and Middle Eastern markets, and similar

transactions in Euro by North American companies on the

European market;

• United Arab Emirates Dirham/Euro: in relation to trade

and financial transactions by Eurozone companies on the

United Arab Emirates market;

• Euro/Norwegian Krone: in relation to trade and financial

transactions by Eurozone companies on the Norwegian

market and vice versa;

• Euro/Danish Krone: in relation to trade and financial

transactions by Eurozone companies on the Danish market

and vice versa;

• Euro/Swedish Krona: in relation to trade and financial

transactions by Eurozone companies on the Swedish

market and vice versa;

• Euro/Canadian Dollar: in relation to trade and financial

transactions by Eurozone companies on the Canadian

market and vice versa;

• Euro/Qatari Riyal: in relation to trade and financial

transactions by Eurozone companies on the Qatari market;

• Turkish Lira/US Dollar: in relation to trade and financial

transactions in US dollars by Turkish companies on foreign

markets and vice versa;

• Euro/Australian Dollar: in relation to trade and financial

transactions by Eurozone companies on the Australian

market and vice versa;

• Euro/Hungarian Forint: in relation to trade and financial

transactions by Hungarian companies on the Eurozone

market and vice versa;

• Brazilian Real/US Dollar: in relation to trade and financial

transactions in US dollars by Brazilian companies on

foreign markets and vice versa.

In 2013, trade and financial flows exposed to these exchange

rates accounted for around 90.9% of the total exposure

to exchange rate risk arising from trade and financial

transactions (90.2% in 2012).

The Group is also exposed to significant exchange rate risks

on the following exchange rates: Euro/Hong Kong Dollar,

Euro/Czech Koruna, Renminbi/US Dollar and Euro/Singapore

Dollar; none of these exposures, taken individually,

accounted for more than 1.6% of the overall exposure to

transactional exchange rate risk in 2013 (1.2% in 2012).

It is the Group’s policy to hedge, where possible, exposures

in currencies other than the accounting currencies of its

individual companies. In particular, the Group hedges:

• Definite cash flows: invoiced trade flows and exposures

arising from loans and borrowings;

• Projected cash flows: trade and financial flows arising

from firm or highly probable contractual commitments.

The above hedges are arranged using derivative contracts.

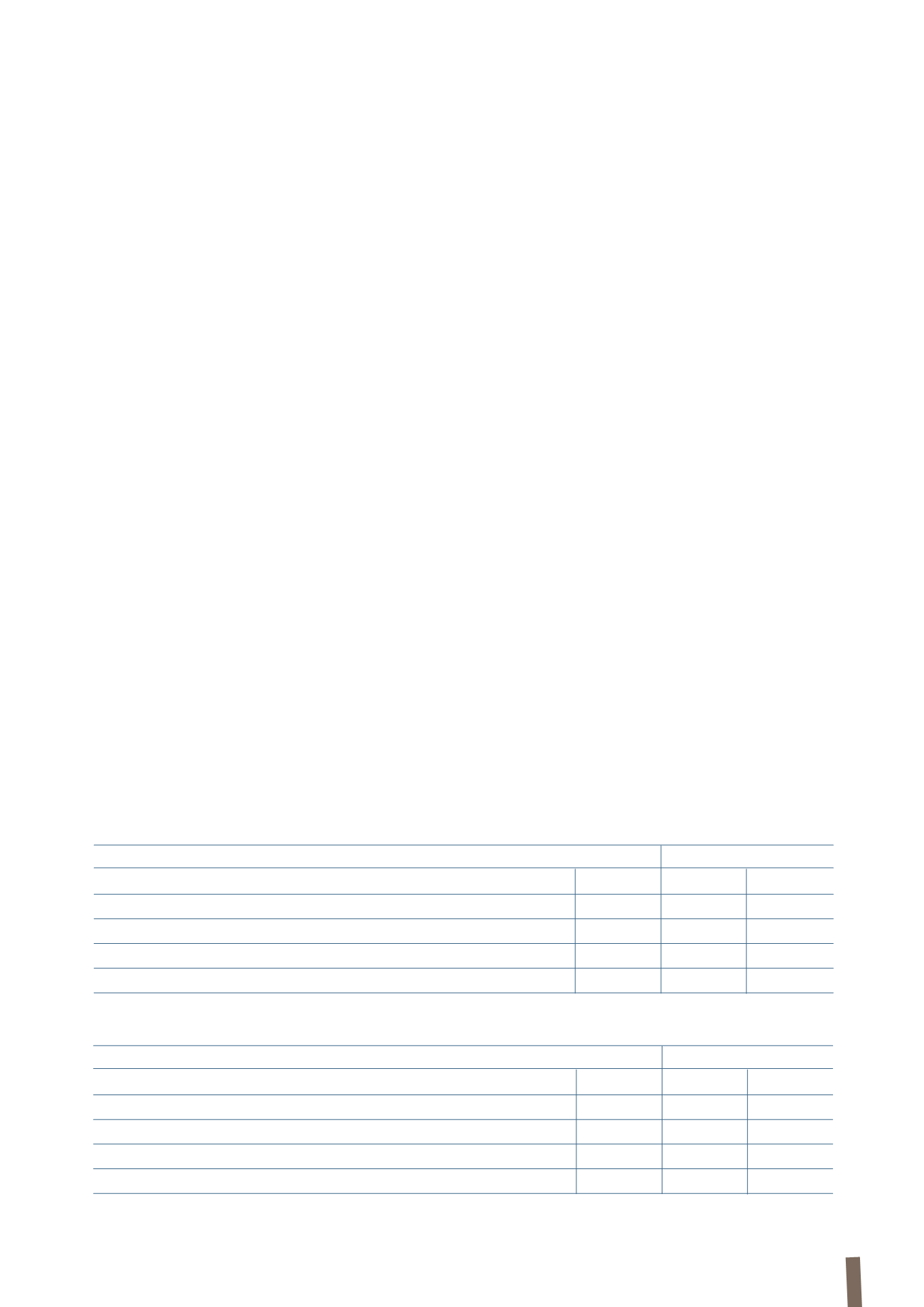

The following sensitivity analysis shows the effects on net

profit of a 5% and 10% increase/decrease in exchange rates

versus closing exchange rates at 31 December 2013 and 31

December 2012.

(in millions of Euro)

2013

2012

-5%

+5%

-5%

+5%

Euro

(1.59)

1.44

(1.13)

1.02

US Dollar

(2.05)

1.85

(1.57)

1.42

Other currencies

(0.71)

0.64

(1.66)

1.51

Total

(4.35)

3.93

(4.36)

3.95

(in millions of Euro)

2013

2012

-10%

+10%

-10%

+10%

Euro

(1.59)

1.44

(1.13)

1.02

US Dollar

(2.05)

1.85

(1.57)

1.42

Other currencies

(0.71)

0.64

(1.66)

1.51

Total

(4.35)

3.93

(4.36)

3.95