PRYSMIAN UPGRADES 2025 GUIDANCE

- THIRD QUARTER IS PRYSMIAN’S BEST EVER: ORGANIC GROWTH AT +9.2%, WITH MARGINS1 (14.8%) AND ADJ. EBITDA (€644 MILLION, +19.3% VS. Q3’24) CONTINUING POSITIVE MOMENTUM

- TRANSMISSION Q3 REVENUES RISE SIGNIFICANTLY (+39.0% ORG. GROWTH), WITH CONTINUED MARGIN ENHANCEMENT REACHING 17.8% (15.3%, Q3’24)

- POWER GRID Q3 ORGANIC GROWTH ACCELERATES (+14.8%) AND ADJ. EBITDA RISES TO €125 MILLION (€119 MILLION, Q3’24)

- INDUSTRIAL & CONSTRUCTION Q3: POSITIVE ORGANIC GROWTH (+2.0%) DRIVEN BY NORTH AMERICA (+10%). SOLID MARGINS AT 14.5%

- CHANNELL HELPS BOOST DIGITAL SOLUTIONS MARGINS (19.6% VS. 14.3%, Q3’24). Q3 ORGANIC GROWTH AT +13.3%

SOLID CASH GENERATION WITH FREE CASH FLOW LTM AT €859 MILLION - SIGNIFICANT ACCELERATION IN RECYCLED CONTENT, REACHING 20.7% (+4.5 P.P. VS. FY24); PERCENTAGE OF

- SUSTAINABLE REVENUES RISES TO 44.4% (43.1%, FY24)

- FY25 OUTLOOK UPGRADED THANKS TO THE EXCELLENT PERFORMANCE OF TRANSMISSION AND THE NORTH AMERICA REGION

Massimo Battaini, Prysmian CEO, said: “Prysmian continues to achieve excellent profitability and revenue growth. The performance in this quarter, the best in Prysmian’s history, underlines that our ‘Accelerating Growth’ strategy places us in the best position to capture all the opportunities in the market while enabling the development and security of both energy and digital infrastructures. This is seen in the performance of Transmission and Power Grid, and the enhanced revenues and profitability in Digital Solutions, also thanks to the contribution from Channell. The continued strength of our I&C business, with solid margins and growing revenues also reflects the benefits that the business has from the exposure to important drivers such as data centers. Thanks to these results, in particular the excellent performance of Transmission and the North America region, we have decided to upgrade the guidance for the second time this year as we continue to increase value for all stakeholders.”

The Board of Directors of Prysmian S.p.A. has approved the Group’s consolidated results for the third quarter, and the first nine months of 2025.

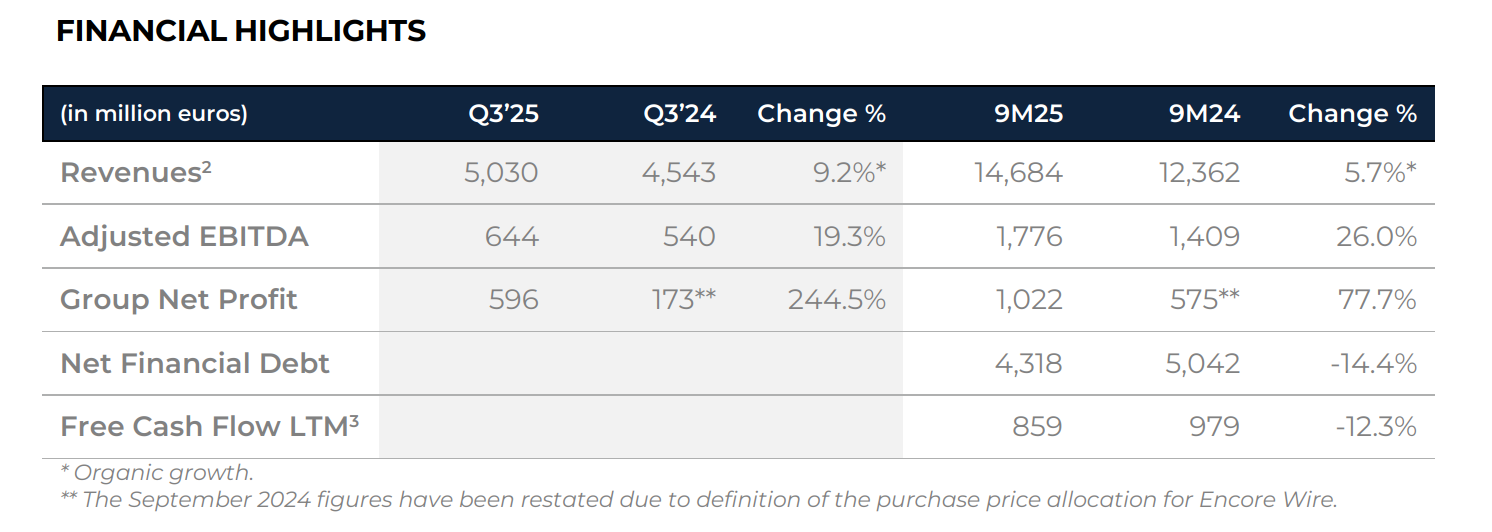

Group Revenues in the third quarter stood at €5,030 million, up from €4,543 million in Q3’24 with +9.2% organic growth. In Q3, Transmission continued its outstanding organic growth (+39.0%), while there was significant acceleration in both Power Grid (+14.8%), reflecting strong performance in North America and Europe, and Digital Solutions (+13.3%). In Electrification, there was organic growth in Industrial & Construction (+2.0%) driven by North America (+10%), while Specialties contracted (-3.0%).

In 9M25, Revenues reached €14,684 million (€12,362 million, 9M24), with +5.7% organic growth.

Revenues reflect the inclusion within the perimeter of both Encore Wire, which was fully consolidated as of July 1, 2024, and Channell, as of June 1, 2025.

Adjusted EBITDA in Q3’25 reached €644 million, up 19.3% compared to €540 million in Q3’24.

The overall margin at standard metal prices was 14.8%, up from 13.8% in Q3’24.

In the third quarter, Transmission’s Adjusted EBITDA rose significantly to €152 million (€92 million, Q3’24), as did the margin, reaching 17.8% (15.3%, Q3’24).

In Power Grid, Adjusted EBITDA was €125 million (€119 million, Q3’24), while the margin was 14.7% (15.2%, Q3’24).

In Electrification, Adjusted EBITDA in Industrial & Construction was €212 million (€211 million, Q3’24), and the margin was solid at 14.5%, in line with Q3’24. In Specialties, Adjusted EBITDA was €70 million (€72 million, Q3’24), while the margin improved to 11.2% (11.1%, Q3’24).

Digital Solutions saw continued profitability expansion, with Adjusted EBITDA almost doubling to €88 million (€45 million, Q3’24), and the margin increased significantly to 19.6% (14.3%, Q3’24), also thanks to the contribution from Channell.

In 9M25, Adjusted EBITDA was €1,776 million (€1,409 million, 9M24) and the margin was 14.1%, up from 13.0% in 9M24.

EBITDA increased in 9M25 to €2,099 million (€1,269 million, 9M24).

Group Net Profit in 9M25 was €1,022 million versus €575 million in 9M24, also thanks to the gain (€354 million) coming from the sale of the stake in YOFC.

Free Cash Flow LTM was €859 million, decreasing versus €979 million LTM in June 2025, mainly due to the different distribution of Transmission cash flows over the quarters.

Net Financial Debt decreased to €4,318 million from €5,042 million at September 30, 2024.

The decrease mainly reflects:

- Free Cash Flow earned in the last twelve months for €859 million generated by:

- €1,880 million net cash flow provided by operating activities (before changes in net working capital);

- €26 million net cash flow absorbed by changes in net working capital;

- €779 million cash outflows for net capital expenditure;

- €226 million payments of net finance costs;

- €10 million dividends received from associates;

- the issued hybrid bond (net effect decreasing net debt for €970 million);

- the proceeds from the sale of the stake in YOFC for €566 million;

- the acquisitions, mainly the Channell and Warren & Brown transactions (+€928 million);

- the share buyback launched in June 2024 (+€210 million);

- the dividend paid to shareholders (+€239 million).

MEDIA & INVESTOR RELATIONS

Maria Cristina Bifulco

Chief Strategy, IR, M&A and Communication Officer

- phone-

- email[email protected]

media relations

Jonathan Heywood

Communication, Public Affairs & Media Relations Director

- phone+39.331.6573546

- email[email protected]