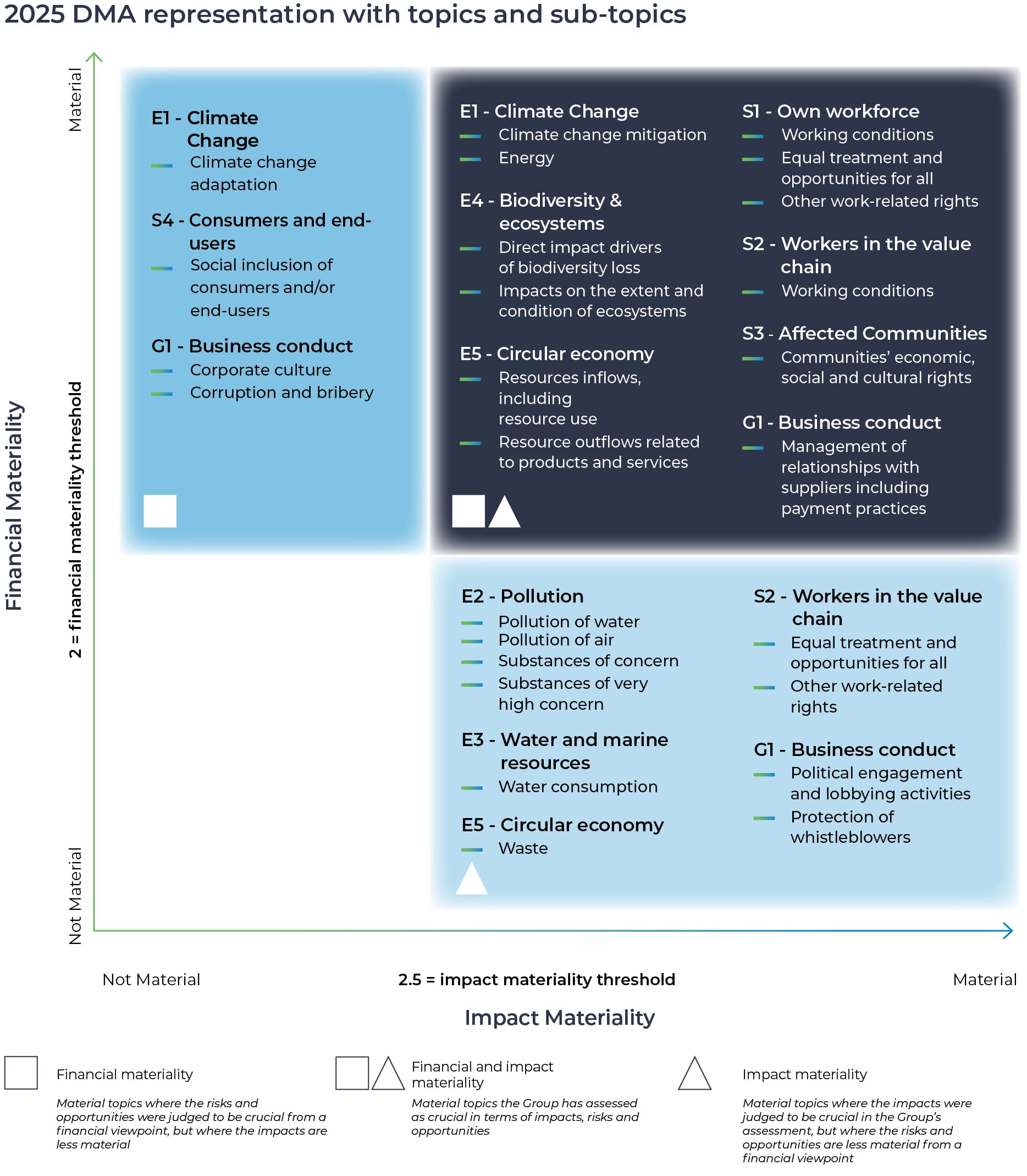

Prysmian’s materiality matrix

For Prysmian, double materiality is a strategic governance tool that enables the Group to integrate sustainability into the definition and development of its “Accelerating Growth” strategy.

Under this approach, the Group carries out a combined assessment of:

- the impact of its own operations on the environment and on people (impact materiality), and

- the risks and opportunities associated with sustainability that may influence the Group’s operating and financial performance (financial materiality).